Few topics in airline distribution generate as much discussion and misunderstanding as the relationship between Global Distribution Systems (GDS) and New Distribution Capability (NDC). The industry conversation is often framed as a transition from GDS to NDC, suggesting a replacement of one model by another. This interpretation misses the point. The real change underway is not about replacing infrastructure, but about redefining control over the airline offer.

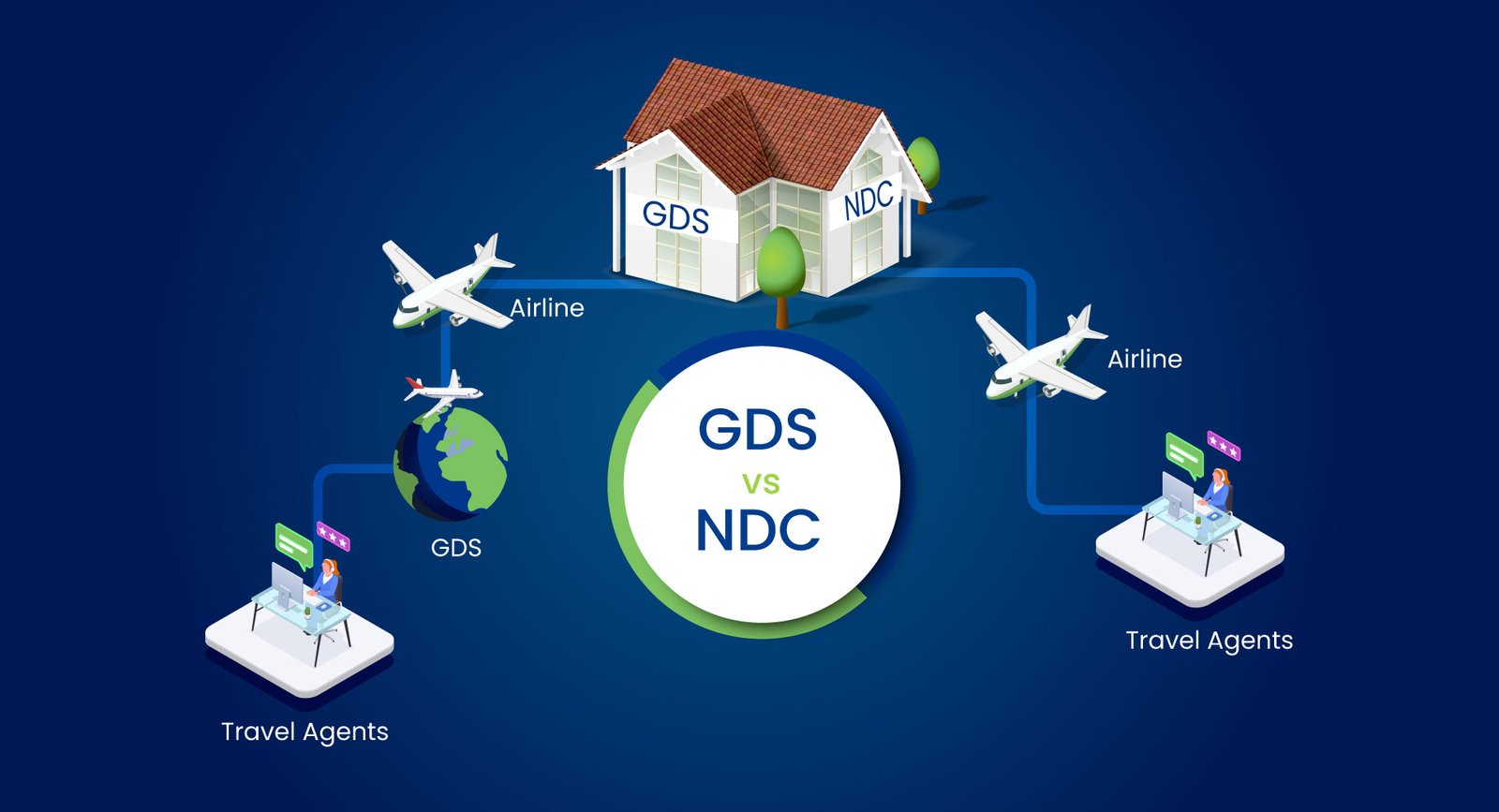

Global Distribution Systems remain the backbone of indirect airline sales. Platforms such as Amadeus, Sabre Corporation and Travelport provide the global marketplace through which airlines distribute content to travel agencies, corporate booking tools and online sellers. Their core value lies in aggregation and scale. Through a single connection, travel sellers can access multiple airlines, compare options efficiently and manage bookings, ticketing, exchanges and reporting within standardized workflows. For corporate travel and high-volume agency environments, this operational consistency remains critical.

NDC plays a fundamentally different role. Developed by the International Air Transport Association (IATA), NDC is a modern data transmission standard designed to transform how airline offers are created and communicated. Instead of distributing pre-filed fares and static inventory, airlines can use NDC to generate dynamic offers in real time. These offers can include bundled services, ancillary products, branded fares, rich media content and increasingly sophisticated pricing logic based on context, demand or customer profile.

The distinction is clear: GDS is distribution infrastructure; NDC is the technology that enables modern airline retailing.

The perception of conflict between the two emerged because NDC gives airlines greater flexibility to connect directly with selected partners. By controlling offer creation at the source, airlines can differentiate products, manage pricing more dynamically and reduce reliance on traditional fare filing processes. Some carriers have reinforced this shift through NDC-only content strategies or differentiated pricing across channels.

However, the industry’s operational reality limits the extent to which direct distribution can scale. Large travel agencies and corporate buyers cannot efficiently manage dozens of separate airline connections while maintaining consistent servicing, reporting and policy compliance. Aggregation remains essential. As a result, GDS providers are evolving their platforms to integrate NDC content alongside traditional EDIFACT content, creating hybrid environments that preserve workflow efficiency while enabling richer airline offers.

This evolution reflects a deeper structural shift. Historically, airline distribution was built around the sale of fares and inventory. Today, airlines are moving toward a retail model in which the primary objective is to control the offer, the combination of price, product, services and presentation delivered to the customer. NDC enables that control. The strategic question is no longer how inventory is distributed, but who manages the logic that creates the offer and how that offer is presented across channels.

For airlines, greater control over offer creation means improved revenue optimization and stronger product differentiation. For travel sellers, the priority remains transparency, comparability and operational efficiency. These priorities are not always aligned. The ongoing transformation of distribution is therefore less about technology adoption and more about the renegotiation of roles, economics and influence across the value chain.

In this context, the idea that NDC will replace the GDS oversimplifies the future. The more likely outcome is a rebalanced ecosystem in which NDC powers airline retail capabilities while aggregation platforms whether traditional GDS or new intermediaries continue to play a central role in scaling distribution.

The real shift in airline distribution is not from GDS to NDC. It is from a system designed around filed fares and inventory to one built around airline-controlled, dynamically constructed offers. As this transition accelerates, the critical questions for the industry will be who controls offer visibility, who influences purchasing decisions and how value is ultimately shared in a more retail-driven distribution environment.

Understanding the difference between GDS and NDC is therefore not just a matter of technology. It is essential to understanding how power, economics and customer ownership are being reshaped across global travel distribution.